Understanding Real Estate Flood Insurance: Coverage, Costs, and Critical Considerations

Introduction: The Overlooked Importance of Flood Insurance in Real Estate

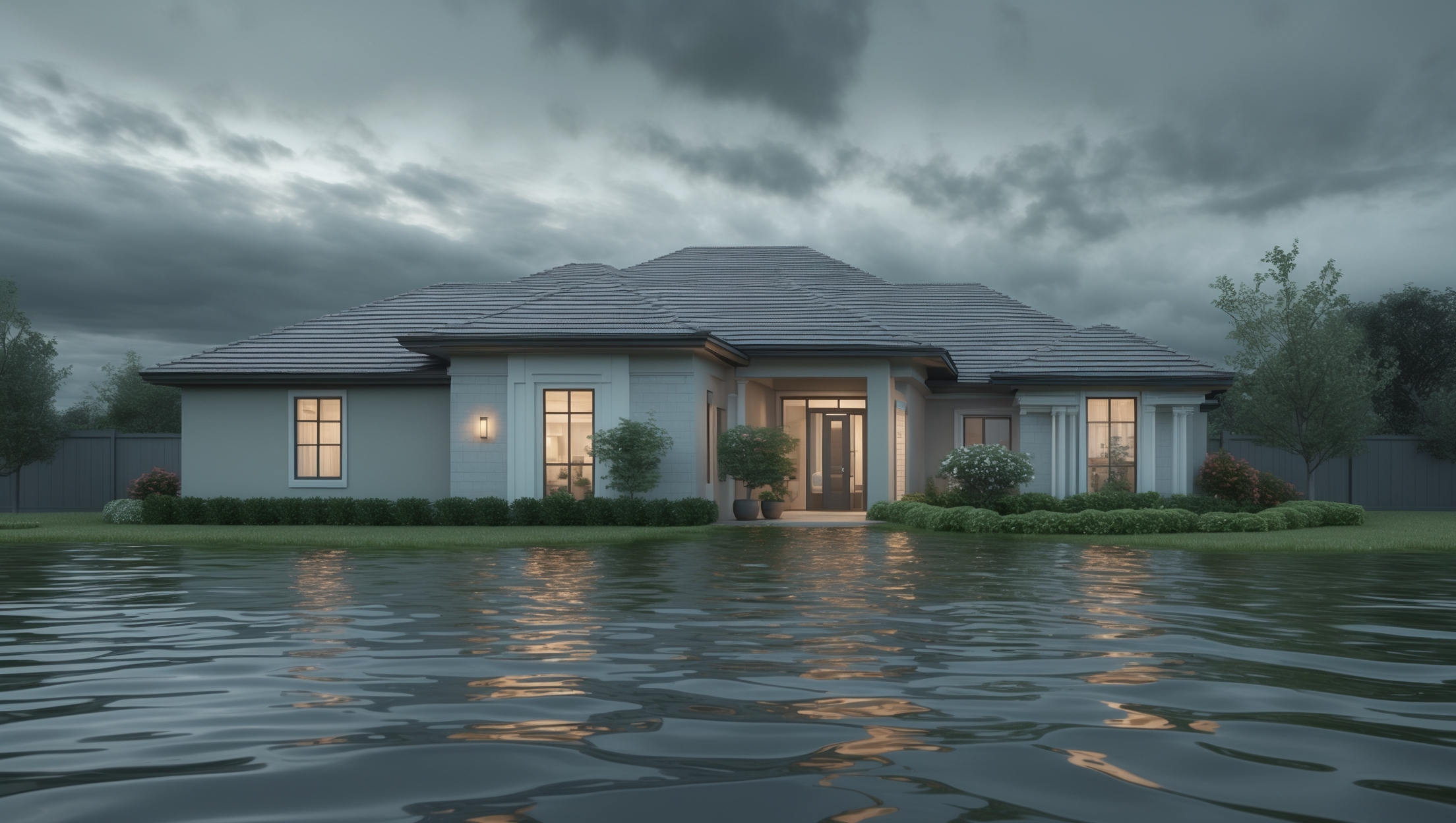

When it comes to protecting your real estate investment, flood insurance is often misunderstood, underestimated, or even ignored until disaster strikes. Many property owners mistakenly believe that standard homeowner’s insurance policies offer flood coverage, only to discover significant gaps in protection after torrential rains or natural disasters. Floods are the most common and costly natural disasters in the United States, affecting both high-risk and moderate-to-low-risk areas. As climate patterns shift and urban development intensifies, the risk of flooding is expanding into regions previously considered safe. Whether you’re a first-time homeowner, a seasoned investor, or a property manager, understanding flood insurance is critical to safeguarding your asset, maintaining compliance with lending requirements, and ensuring your financial resilience. This comprehensive guide demystifies real estate flood insurance, covering what it is, how it works, compliance obligations, cost factors, and strategic considerations for property owners. By the end, you’ll be equipped to make informed decisions that could protect your property—and your peace of mind—when the unexpected happens.

What Is Flood Insurance? Defining Coverage and Scope

The Distinction from Standard Homeowner’s Insurance

Standard homeowner’s and commercial property insurance policies typically exclude flood damage. Flood insurance is a separate policy, designed to cover losses caused specifically by flooding events such as heavy rain, coastal storm surges, snowmelt, blocked storm drainage, or the overflow of inland or tidal waters. Without a dedicated flood policy, you risk substantial out-of-pocket expenses to repair or rebuild after a flood event.

What Qualifies as a Flood?

The National Flood Insurance Program (NFIP) defines a flood as “a general and temporary condition of partial or complete inundation of two or more acres of normally dry land area or of two or more properties.” This includes events like:

- Overflow of inland or tidal waters

- Unusual and rapid accumulation or runoff of surface waters

- Collapse or subsidence of land along the shore of a lake or similar body of water due to erosion or undermining caused by waves or currents exceeding anticipated cyclical levels

Types of Flood Insurance Policies

- NFIP Policies: The majority of flood insurance is provided through the federally backed National Flood Insurance Program, managed by FEMA and available through participating insurers.

- Private Flood Insurance: Some insurers offer private flood policies, often with broader coverage limits or additional features not available through NFIP.

Flood Insurance Coverage: What’s Included and What’s Not

Structural Coverage

Flood insurance typically covers:

- The building and its foundation

- Electrical and plumbing systems

- Central air conditioning, furnaces, and water heaters

- Refrigerators, stoves, and built-in appliances

- Permanently installed carpeting over unfinished floors

- Detached garages (limited coverage)

Contents Coverage

Separate or additional coverage for personal property may include:

- Personal belongings (clothes, furniture, electronics)

- Portable appliances

- Washer and dryer

- Window air conditioners

- Valuable items (subject to sub-limits)

What Flood Insurance Does Not Cover

There are important exclusions to note:

- Damage caused by moisture, mildew, or mold not directly attributable to floodwater

- Property and belongings outside the insured building (decks, patios, landscaping, fences, pools)

- Living expenses, such as temporary housing or loss of income

- Cars and vehicles (these require separate auto insurance)

- Basement improvements (finishing, carpeting, wall coverings)

- Currency, precious metals, stock certificates

Who Needs Flood Insurance? Risk Assessment and Compliance

Mandatory Purchase Requirements

If your property is located in a Special Flood Hazard Area (SFHA) and you have a federally-backed mortgage, you are legally required to purchase flood insurance. Lenders enforce this requirement to protect their collateral against catastrophic loss.

Assessing Flood Risk: Beyond the Maps

Flood risk is determined by FEMA’s Flood Insurance Rate Maps (FIRMs), which classify areas into risk zones. However, more than 20% of NFIP claims come from properties outside high-risk zones, underscoring the value of coverage even in moderate- or low-risk areas. Consider:

- Proximity to rivers, lakes, or coastlines

- Local drainage infrastructure

- Elevation and topography

- Recent construction or land development

- History of flooding in the area

Voluntary Coverage for Low- and Moderate-Risk Properties

Even if not required, flood insurance can be an affordable hedge against unexpected disasters for properties outside SFHAs. Preferred Risk Policies (PRPs) are available for eligible low-risk properties at reduced rates.

How Much Does Flood Insurance Cost?

Premium Factors

The cost of flood insurance varies widely and is influenced by:

- Location and flood zone designation

- Building occupancy and type (residential, commercial, multi-family)

- Year of construction and building elevation

- Number of floors and presence of a basement

- Coverage amount and deductible selected

- Community participation in NFIP and local mitigation efforts

Average Premium Ranges

As of 2024, average NFIP premiums for residential properties range from $700 to $1,400 annually, but premiums for high-risk properties can exceed $2,500 per year. Private insurers may offer different rates, often with higher coverage limits or lower deductibles.

Deductibles and Out-of-Pocket Costs

Flood insurance policies allow you to choose deductibles for building and contents coverage, typically ranging from $1,000 to $10,000. Higher deductibles lower your premium but increase your out-of-pocket costs after a flood.

Key Steps to Obtaining Flood Insurance

Step 1: Assess Your Risk and Insurance Needs

Start by reviewing FEMA flood maps, consulting with local officials, and evaluating the property’s history and risk profile. If your mortgage requires coverage, confirm the minimum requirements.

Step 2: Compare Policy Options

- Contact your existing property insurer to inquire about NFIP policies.

- Request quotes from private flood insurers for comparison.

- Evaluate policy limits, deductibles, exclusions, and premium costs.

Step 3: Gather Required Documentation

- Flood zone determination letter

- Elevation Certificate (may be needed for rate calculation, especially in high-risk zones)

- Property details (year built, construction type, foundation type, square footage)

Step 4: Purchase and Maintain the Policy

Once you select a provider and policy, complete the application and ensure timely payment. Note that there is typically a 30-day waiting period before coverage takes effect (except for new mortgages or certain map changes).

Understanding Claims: Filing and Recovery After a Flood

Documenting Damage

After a flood event:

- Take photographs and videos of all affected areas and items.

- Make a detailed inventory of damaged property.

- Contact your insurer immediately to start the claims process.

Working with Adjusters

An insurance adjuster will inspect the damage. Be present to answer questions and provide documentation. Keep receipts for any emergency repairs or mitigation expenses.

Payouts and Recovery

NFIP policies pay for actual cash value (depreciated) of most contents, and replacement cost or actual cash value for buildings, depending on policy type and eligibility. Review settlement offers carefully and appeal if necessary.

Compliance and Regulatory Considerations

Lender Requirements and Flood Zone Changes

Lenders may require you to maintain flood coverage for the life of the loan. If flood maps change and your property is newly designated high-risk, you may be required to obtain coverage, even mid-loan. Periodically review your flood zone status and communicate with your lender to avoid lapses.

Community Rating System (CRS) Discounts

Some communities participate in the NFIP’s Community Rating System, which rewards local flood mitigation efforts with premium discounts for property owners. Check with your municipality for eligibility and potential savings.

Building Codes and Mitigation Measures

Local building codes may require flood-resistant construction techniques or elevation of structures. Compliance can affect your eligibility for insurance and may lower your premium.

Smart Strategies for Real Estate Owners and Investors

Mitigation to Lower Risk and Premiums

- Elevate electrical systems, HVAC equipment, and critical utilities above base flood elevation (BFE).

- Install flood vents in crawl spaces and garages.

- Use flood-resistant materials for floors, walls, and insulation.

- Landscape with grading and drainage improvements to direct water away from structures.

- Maintain gutters, downspouts, and storm drains to reduce accumulation around the foundation.

Regular Policy Review and Updates

Annually review your flood policy to ensure coverage keeps pace with property improvements, inflation, and changing risk. Update your insurer on renovations or mitigation work which could qualify you for lower premiums.

Leverage Flood Insurance in Real Estate Transactions

- For Sellers: Disclose flood zone status and provide copies of flood insurance policies and claims history. Highlight mitigation efforts as selling points.

- For Buyers: Request the seller’s Elevation Certificate and claims history. Factor expected premiums into your budget.

- For Investors: Compare properties based on total cost of ownership, including flood insurance and potential risk.

Common Myths and Misconceptions About Flood Insurance

- Myth: “I’m not in a high-risk zone, so I don’t need flood insurance.”

Fact: Floods can happen anywhere. One in three disaster assistance claims come from outside high-risk areas. - Myth: “Federal disaster aid will cover my losses.”

Fact: Most disaster assistance is a loan that must be repaid, and is only available if a federal disaster is declared. - Myth: “Flood insurance is too expensive.”

Fact: Premiums for low-risk properties can be surprisingly affordable, and the cost of rebuilding far exceeds the annual premium. - Myth: “If my property has never flooded, it never will.”

Fact: Past performance does not guarantee future results, especially with changing weather patterns and urban development.

Conclusion: Safeguarding Your Real Estate Investment

Flood insurance remains one of the most critical—and often overlooked—components of a comprehensive real estate risk management strategy. Whether mandated by your lender or pursued voluntarily, it provides a financial safety net that can mean the difference between recovery and financial ruin in the wake of a flood. The process of obtaining the right coverage requires diligence: understanding what’s covered and what’s not, accurately assessing your property’s risks, and regularly reviewing your policy as your circumstances and local flood maps change. Don’t let common myths lull you into a false sense of security—flooding is a real threat even in areas deemed low risk, and standard insurance policies simply don’t fill the gap.

Take a proactive approach by integrating flood risk assessment into your property management and acquisition process. Invest in mitigation measures not only to safeguard your building but also to potentially lower your premiums. For sellers and buyers alike, flood insurance details should be a transparent part of every transaction. Remember, the true value of flood insurance lies not just in compliance, but in the peace of mind it delivers when you need it most. By making informed decisions today, you can ensure that your real estate investment stands strong against the unpredictable forces of nature tomorrow.

Could you clarify if flood insurance policies cover damage caused by heavy rain that seeps in through basement walls, or is that excluded since some insurance providers might define flood a bit differently?

Flood insurance policies typically cover damage from flooding caused by events like overflowing rivers, heavy rain causing surface water to enter the home, or storm surges. However, if water seeps into your basement through walls due to heavy rain but there’s no general flooding of the area, most policies consider that seepage and often exclude it. Always review your specific policy details or speak with your provider, since definitions and coverage can vary.

The article says floods can affect even moderate-to-low-risk areas. How do I accurately determine whether my property is in a flood zone that requires insurance, and is this information updated regularly based on changing climate patterns?

To find out if your property is in a flood zone requiring insurance, check FEMA’s Flood Insurance Rate Maps or contact your local government’s planning department. These maps are periodically updated to reflect new data and changing environmental factors, including climate trends. It’s a good idea to review your property’s status every few years or after significant local weather events to stay current.